Can’t-Miss Takeaways Of Info About Examples Of Journal Entries With Ledger And Trial Balance

Divine 15 Transactions With Their Journal Entries Ledger Trial Balance

Practical 1 Journal, Ledger And Trial Balance Youtube

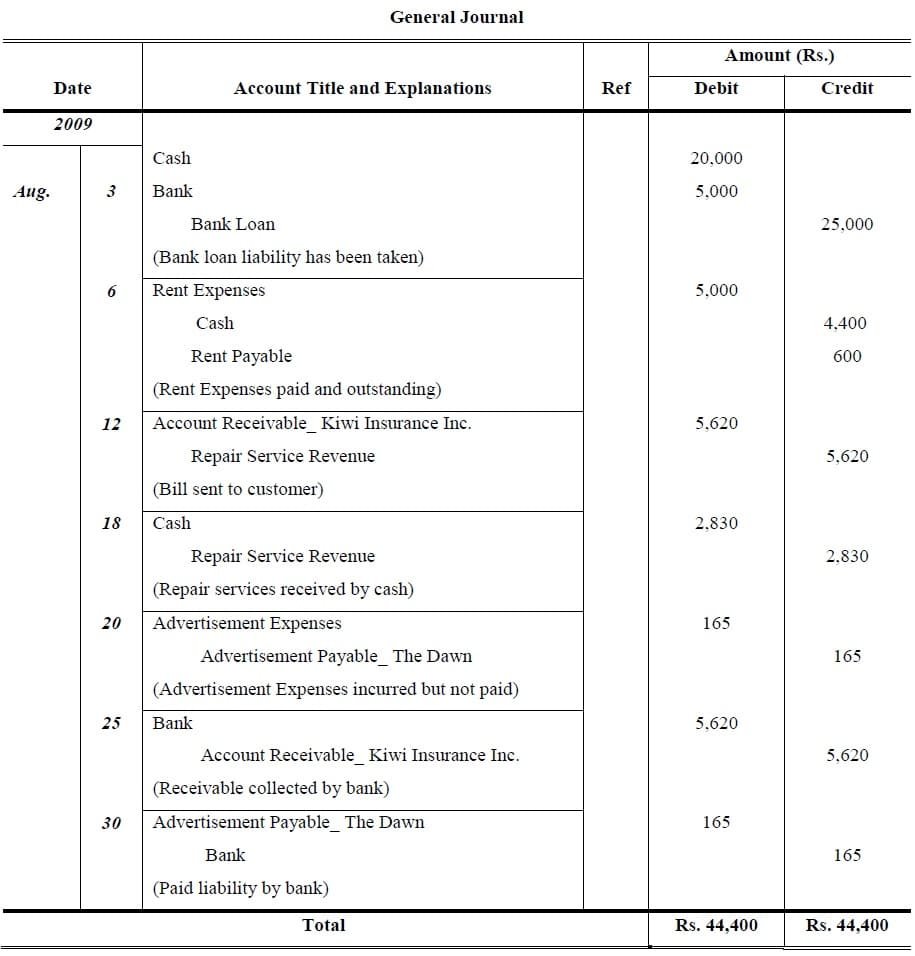

General Journal And Ledger Entries Accounting Corner

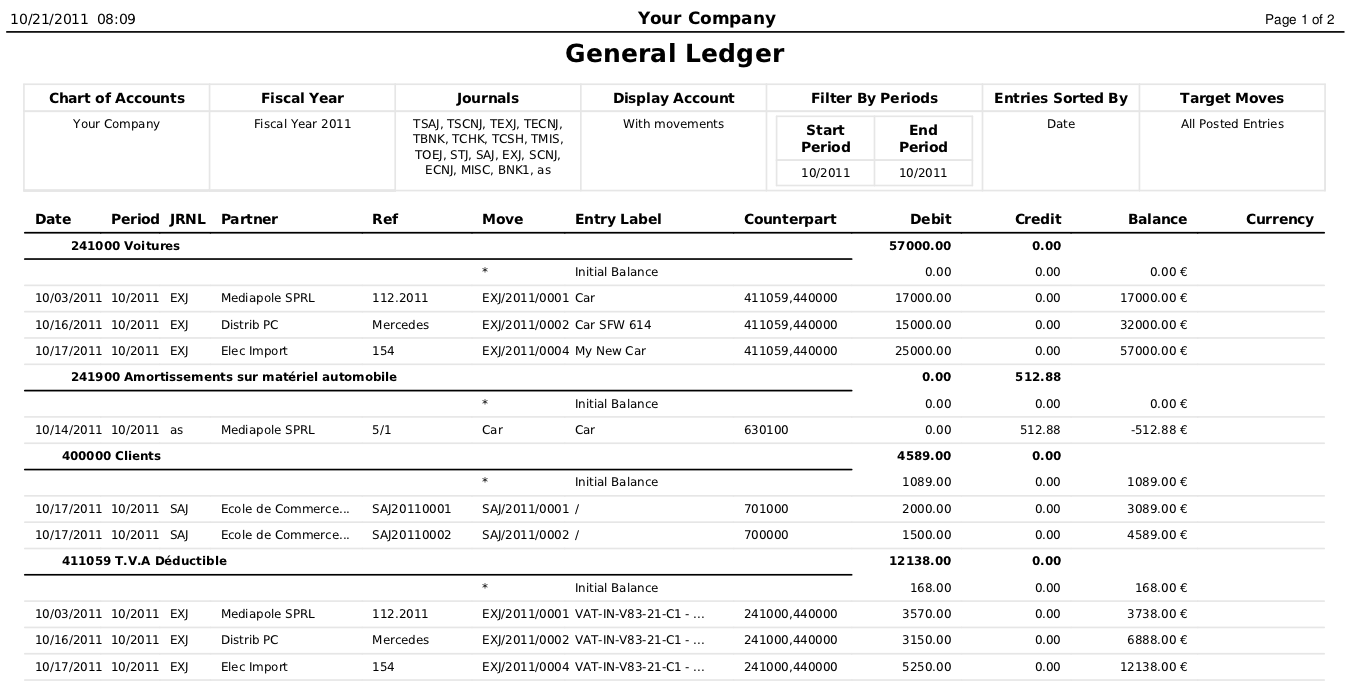

General Ledger Examples I Format Accountancy Knowledge

Journal Entries Ledger Trial Balance Problem And Solution Google Sheets

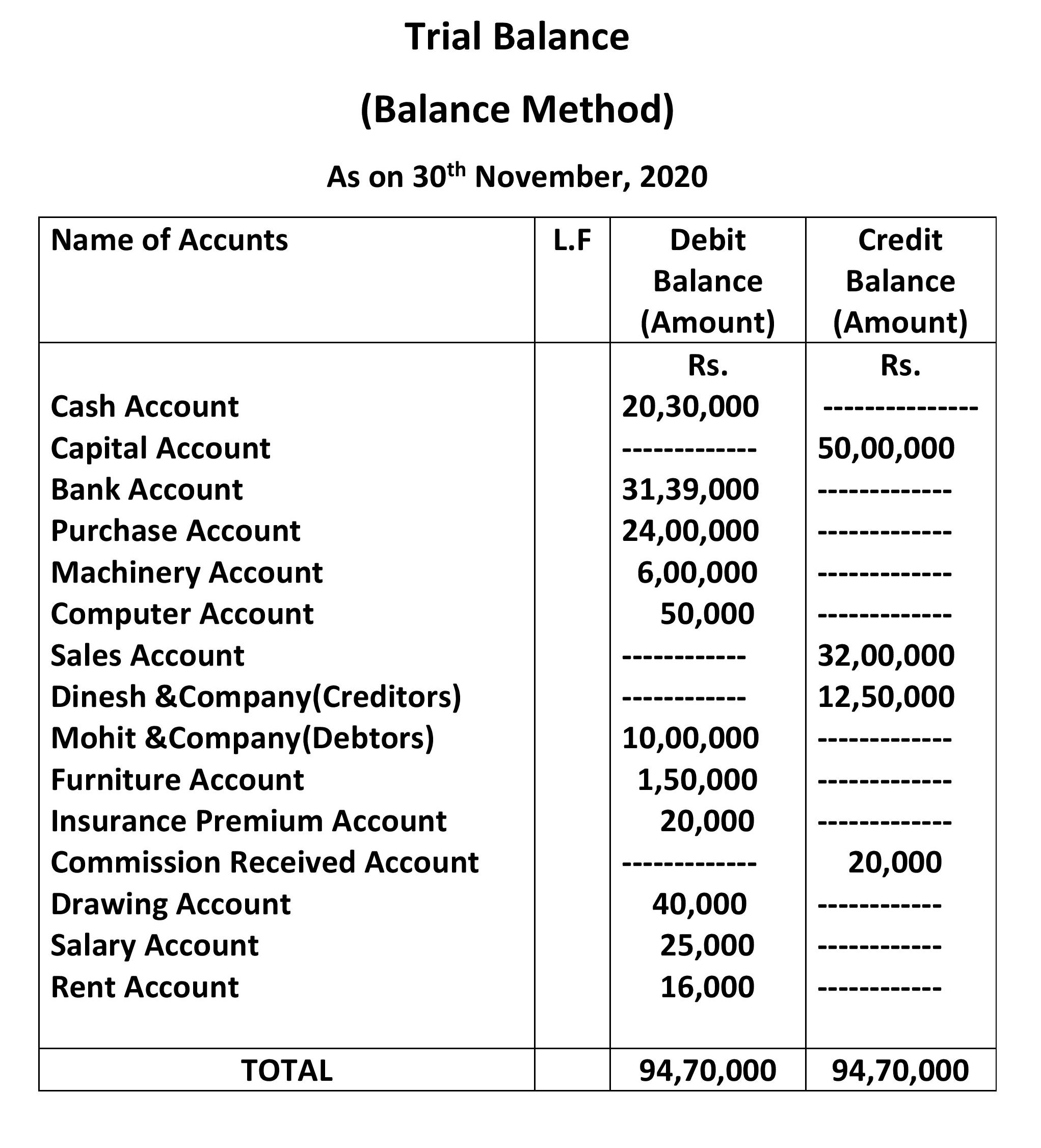

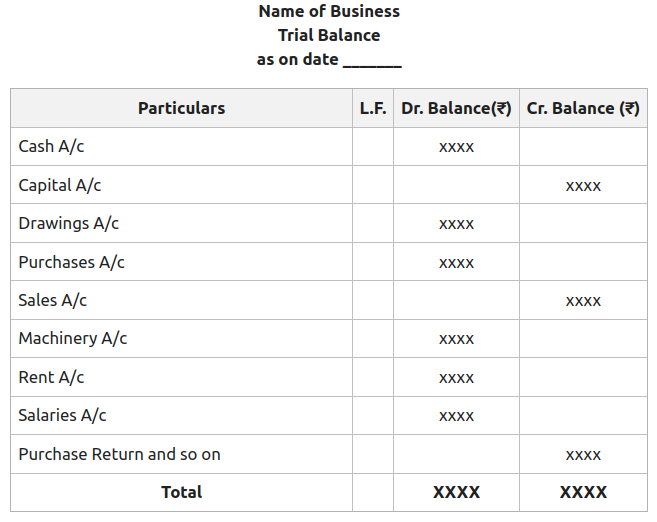

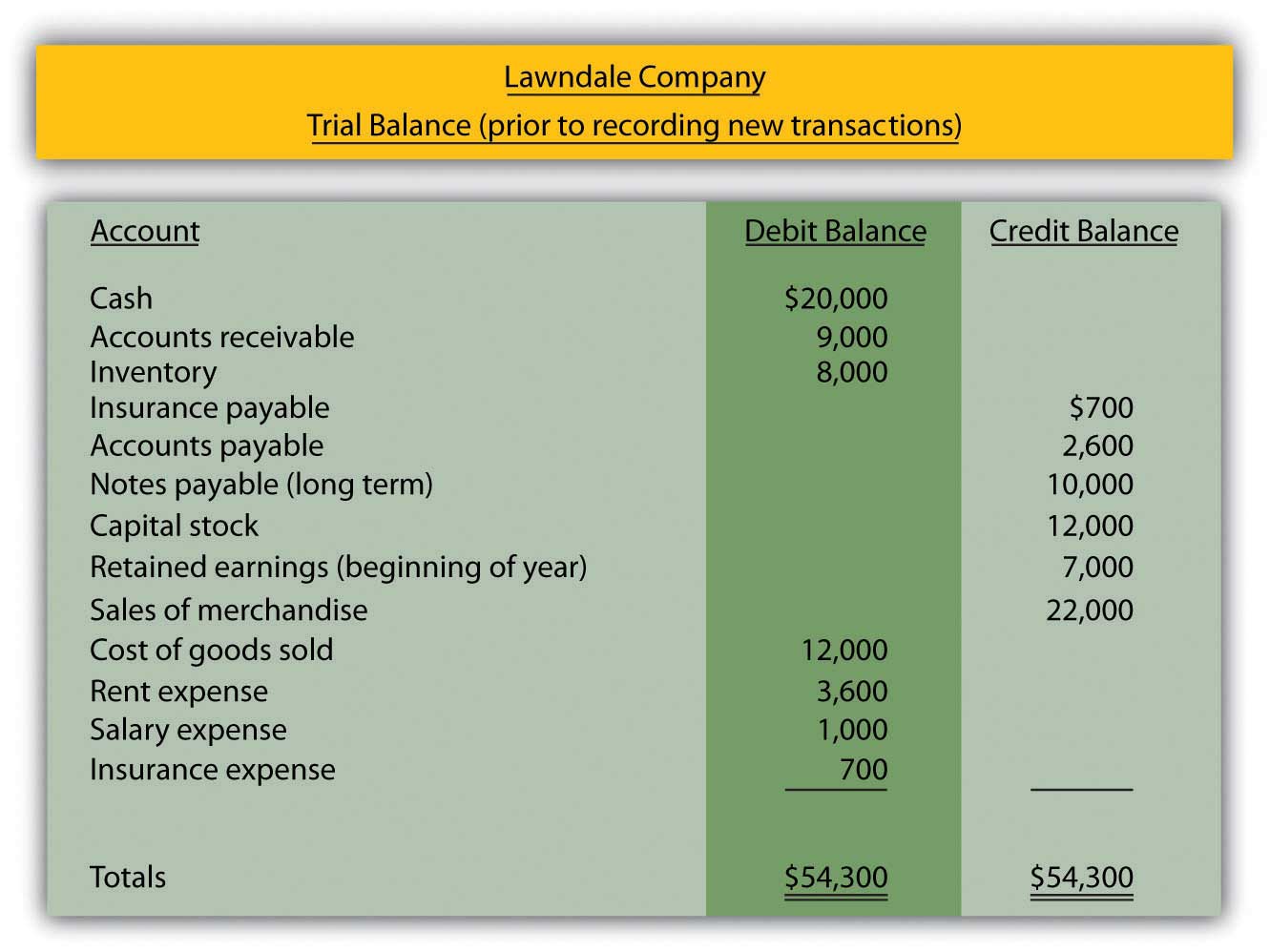

Trial Balance Format

It is not taken from previous examples but is intended to stand alone.

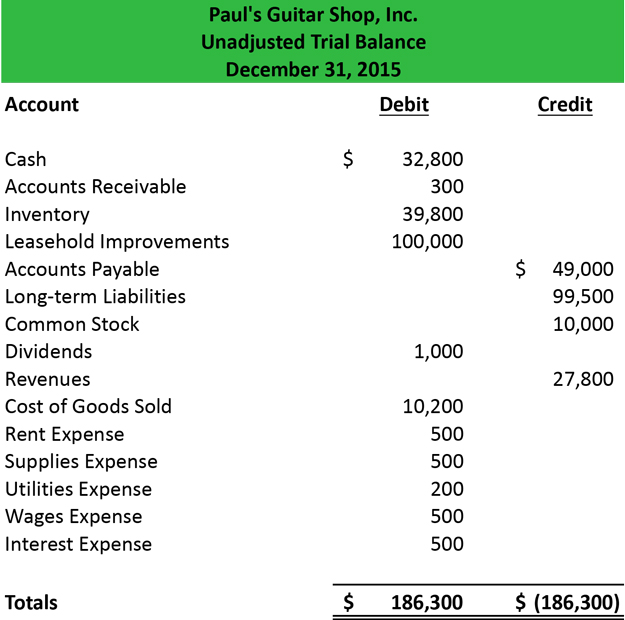

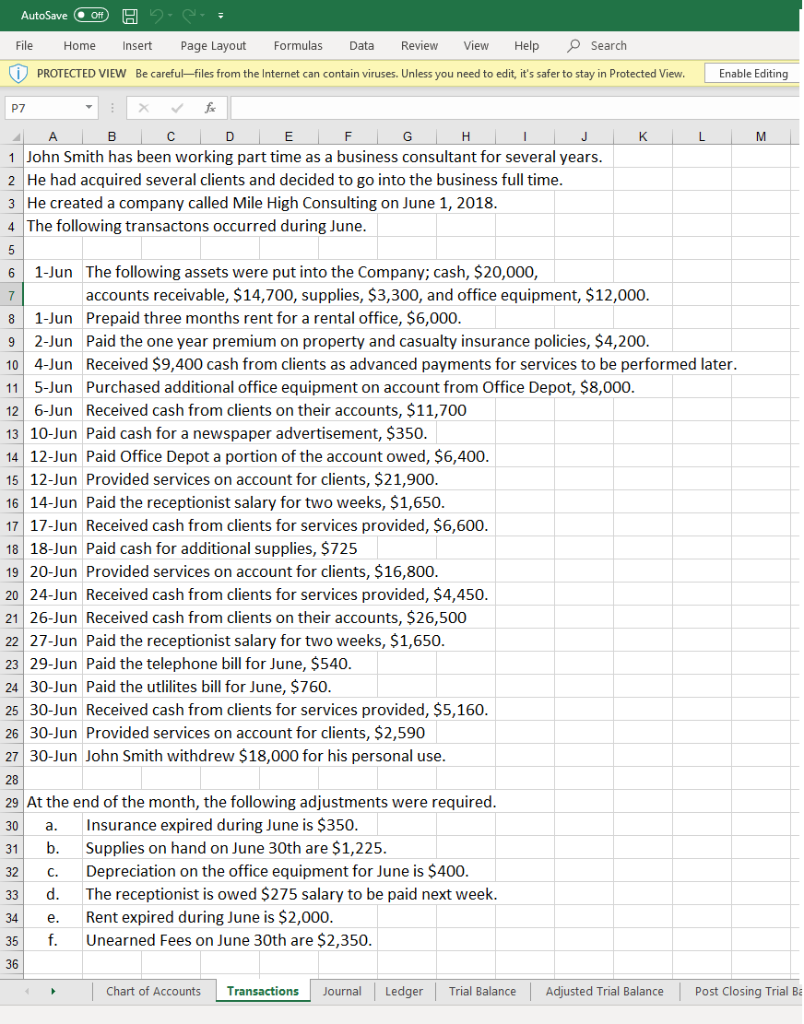

Examples of journal entries with ledger and trial balance. Professor aj kooti provides a detailed examples of how to use t accounts and enter journal entries into the trial balance. It is prepared again after the adjusting entries are posted to ensure that the total debits and credits are still balanced. Preparing an unadjusted trial balance is the fourth step in the accounting cycle.

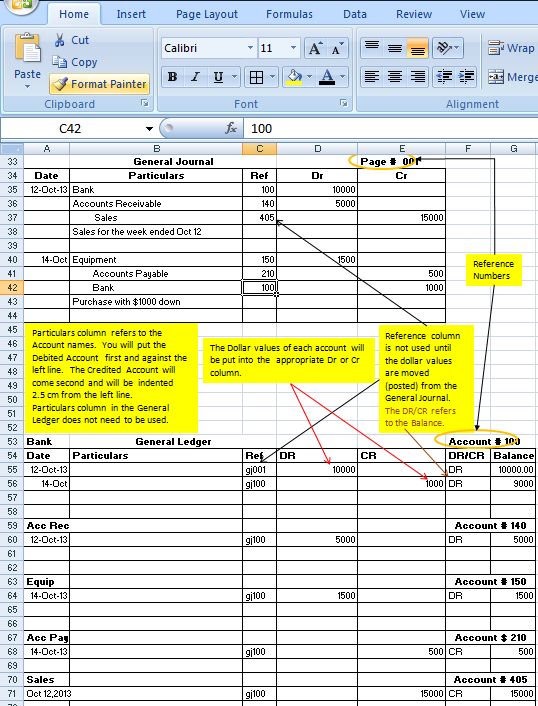

The journal entry may also include a reference number, such as a check number, along with a. Journal, ledger and trial balance (financial accounting) in this article, we will discuss the basic concepts of financial accounting i.e. A ledger is where the entries related to a particular account are recorded.

This has been a guide to ledger account examples. All the journal entries recorded in the journal are posted to the ledgers. Credited as per the golden rules of accounting.

Journal is not balanced while ledger accounts are balanced. A journal entry (also known as a general journal) include the following information about a transaction: Ledger entries are not supported by narrations.

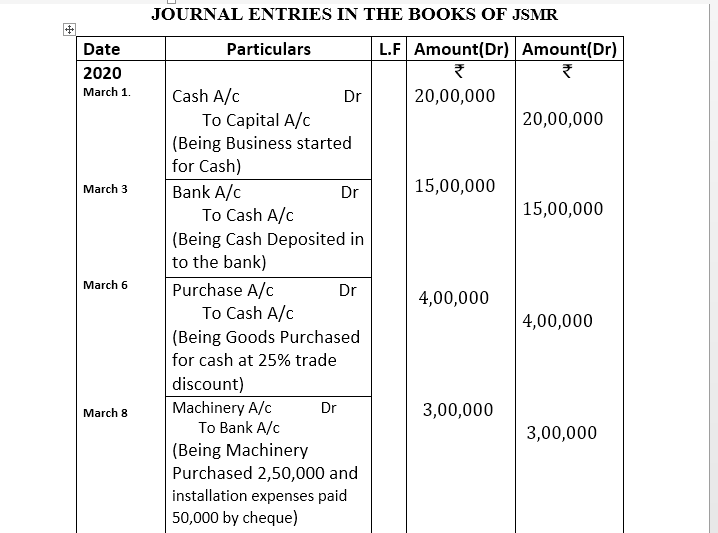

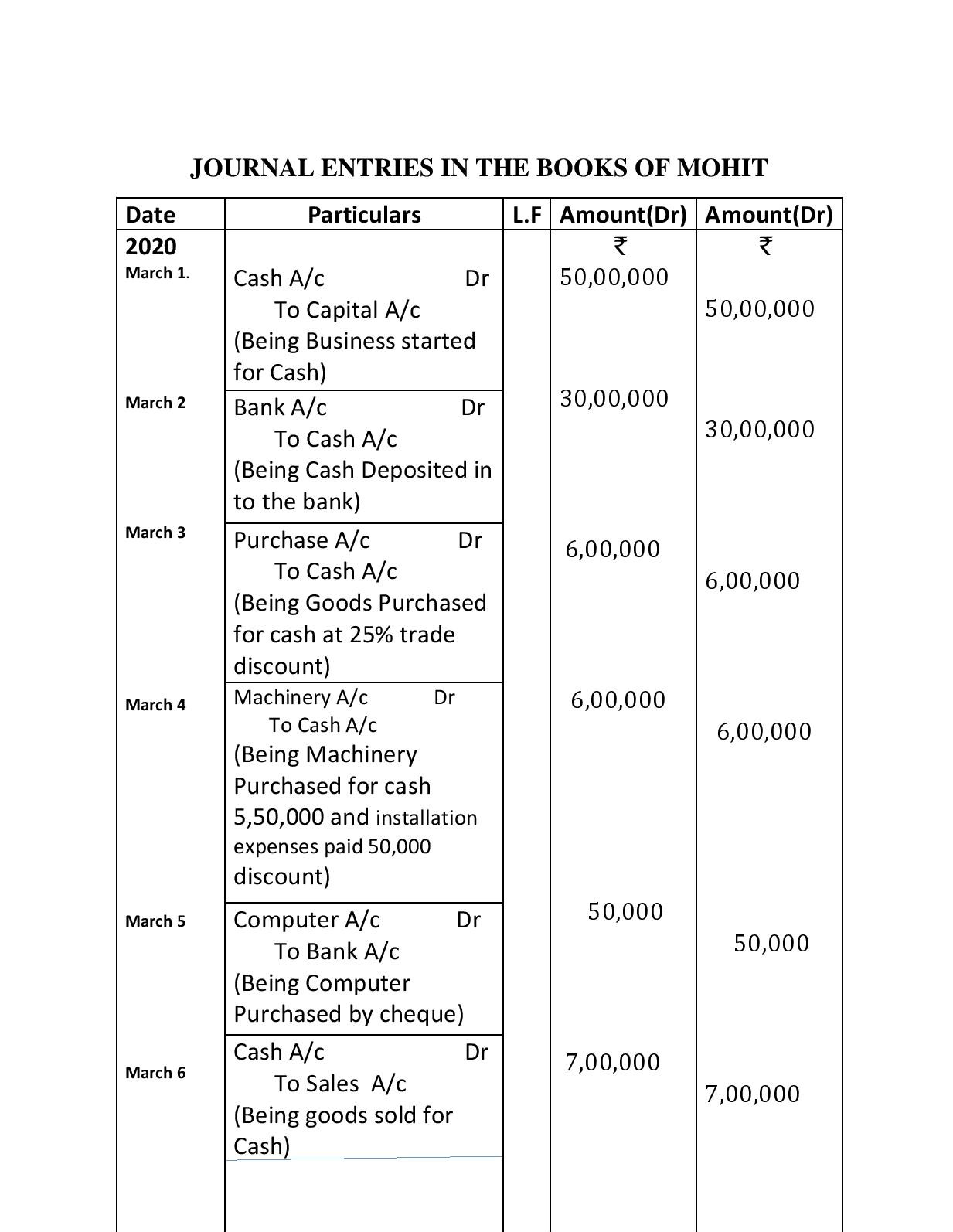

Journal, ledger, and trial balance as per financial accounting rules. The accounts to be debited and credited; Cash a/c and capital a/c.

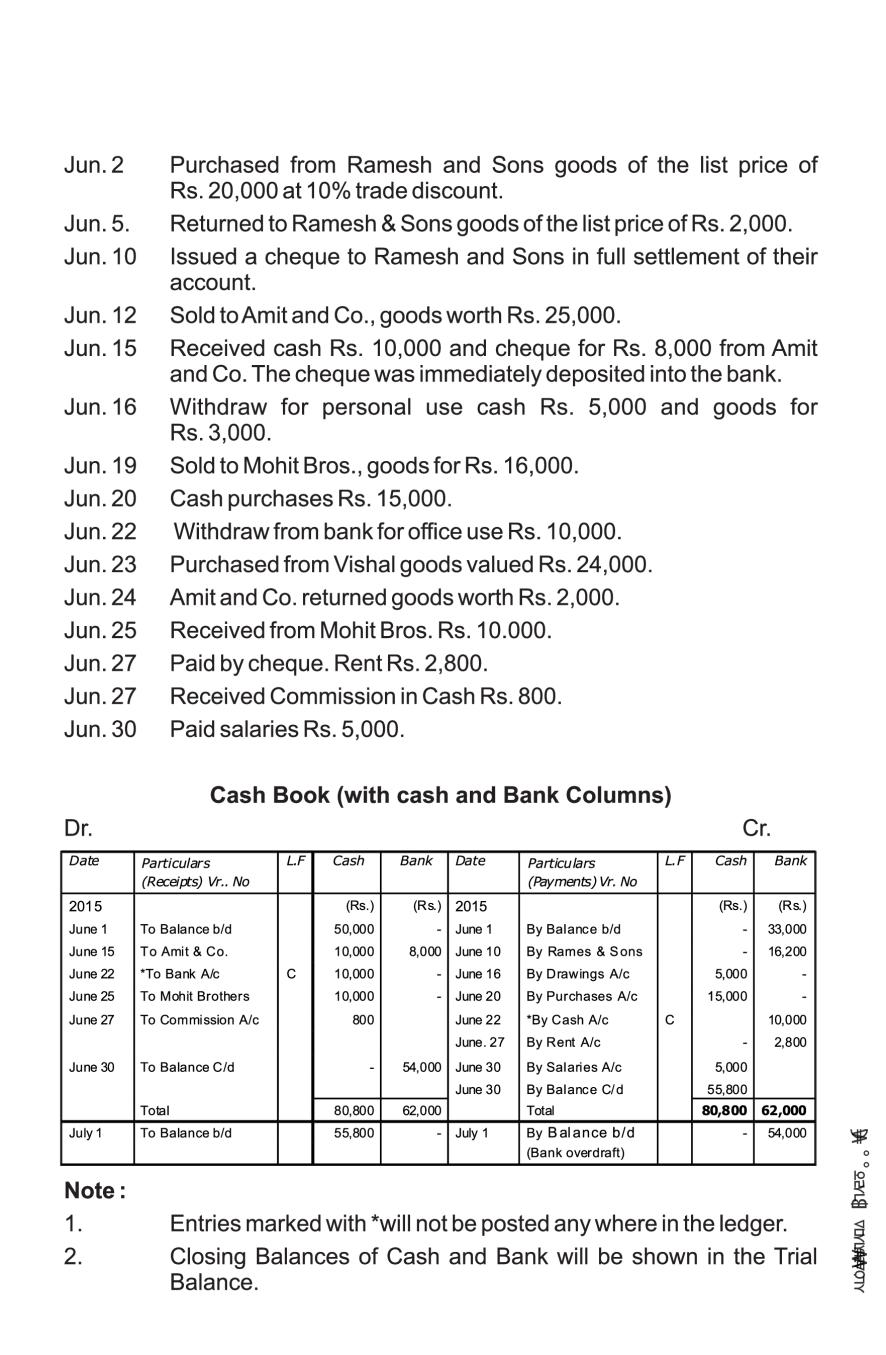

The date of the transaction; For example, all the transactions related to salary will be recorded in the salary account ledger. 20 transactions with their journal entries, ledger and trial balance

Formatting when recording journal entries For example, utility expenses during a period include the payments of four different bills amounting to $ 1,000, $ 3,000, $ 2,500, and $ 1,500, so in the trial balance, single utility expenses account will be shown wi. Discover the meaning of a journal entry and a trial balance, types of journal entries, how a general ledger differs from a trial balance, and some examples.

In this topic, we also cover how to prepare journal, ledger, and trial balance with practical problems and solutions. For example, the trial balance may balance even when any of the following occurs: Here we discuss the most common examples of ledger accounts and journal entries and explanations.

The process of transferring the debits and credits from the journals to the. It has a list of all the general ledger accounts contained in the ledger of a business. (a) a transaction is not journalised (b) a journal entry is posted twice (c) errors are made in recording the amount of a transaction (d) a correct journal entry is not posted to the ledger (e) incorrect accounts are used in journalising or posting.

Errors revealed by trial balance trial balance, as we know, is a statement prepared after the ledger, followed by a journal. A brief explanation of each transaction; Every journal entry in the general ledger will include the date of the transaction, amount, affected accounts with account number, and description.

Accounting An Introduction The General Journal & Ledger

Outstanding 30 Journal Entries With Ledger Trial Balance And Final

30 Transactions With Their Journal, Ledger, Trial Balance And Final

Contoh Bank Reconciliation Data Dikdasmen

Unadjusted Trial Balance Format Preparation Example

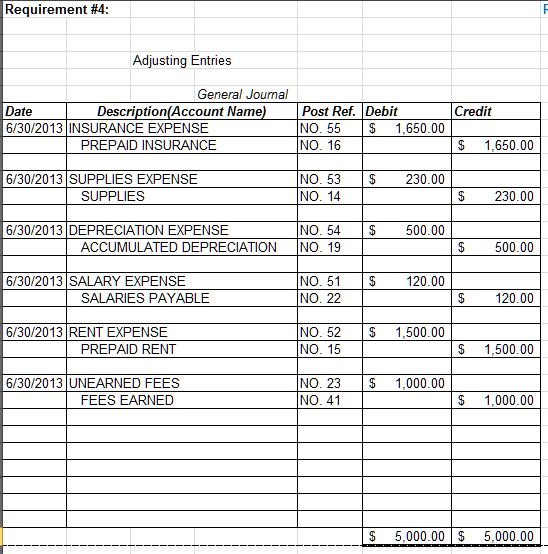

Solved 1. Prepare/journalize The Adjusting Entries Af A.

Outstanding 30 Journal Entries With Ledger Trial Balance And Final

General Ledger A Complete And Simple Guide

Journals And Ledgers In Bookkeeping Zoho Books

Trial Balance Accounting Play

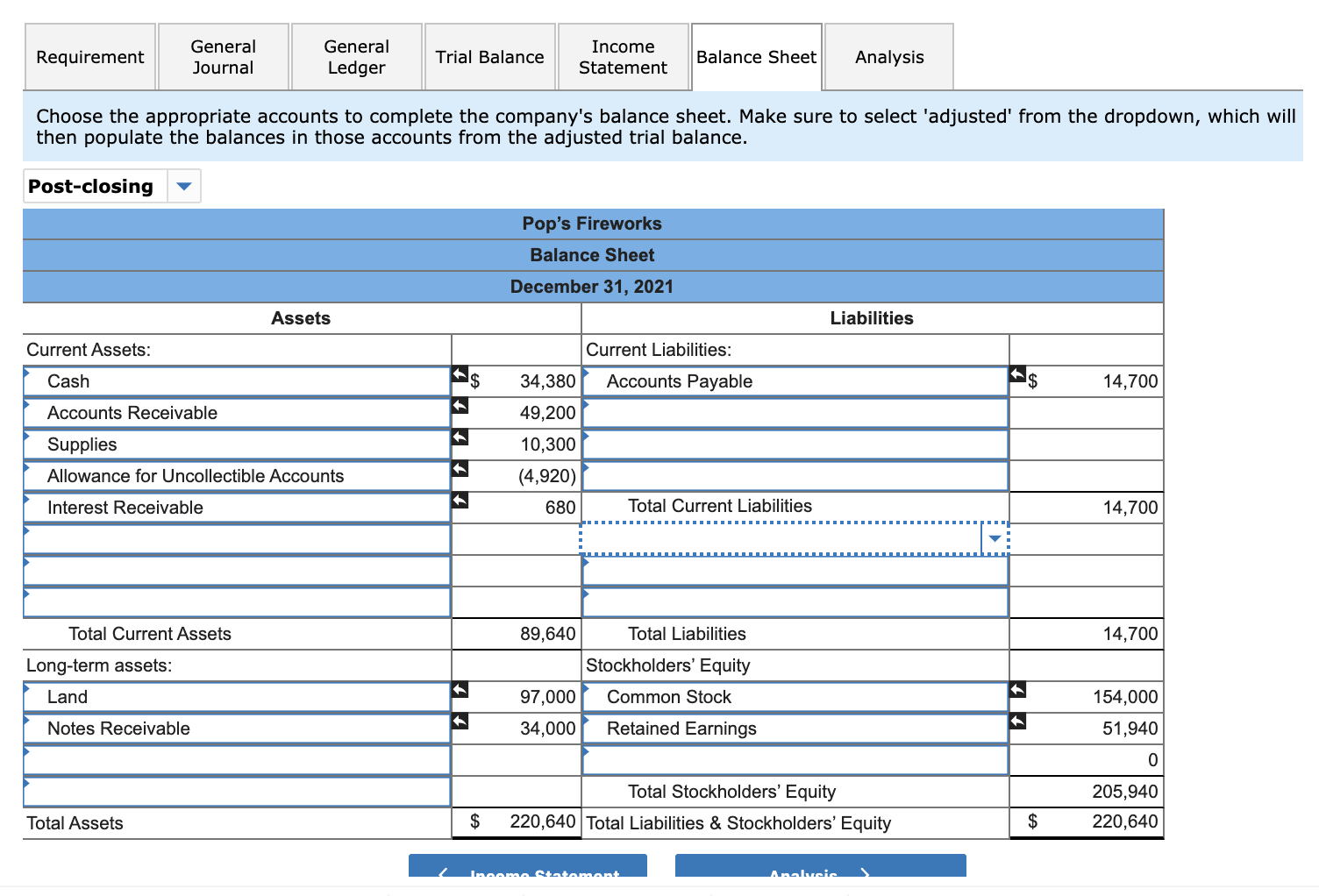

Solved Requirement General Journal Ledger Trial