Inspirating Tips About Statement Of Profit And Loss Other Comprehensive Income Format

Statement Of Comprehensive Overview, Components And Uses

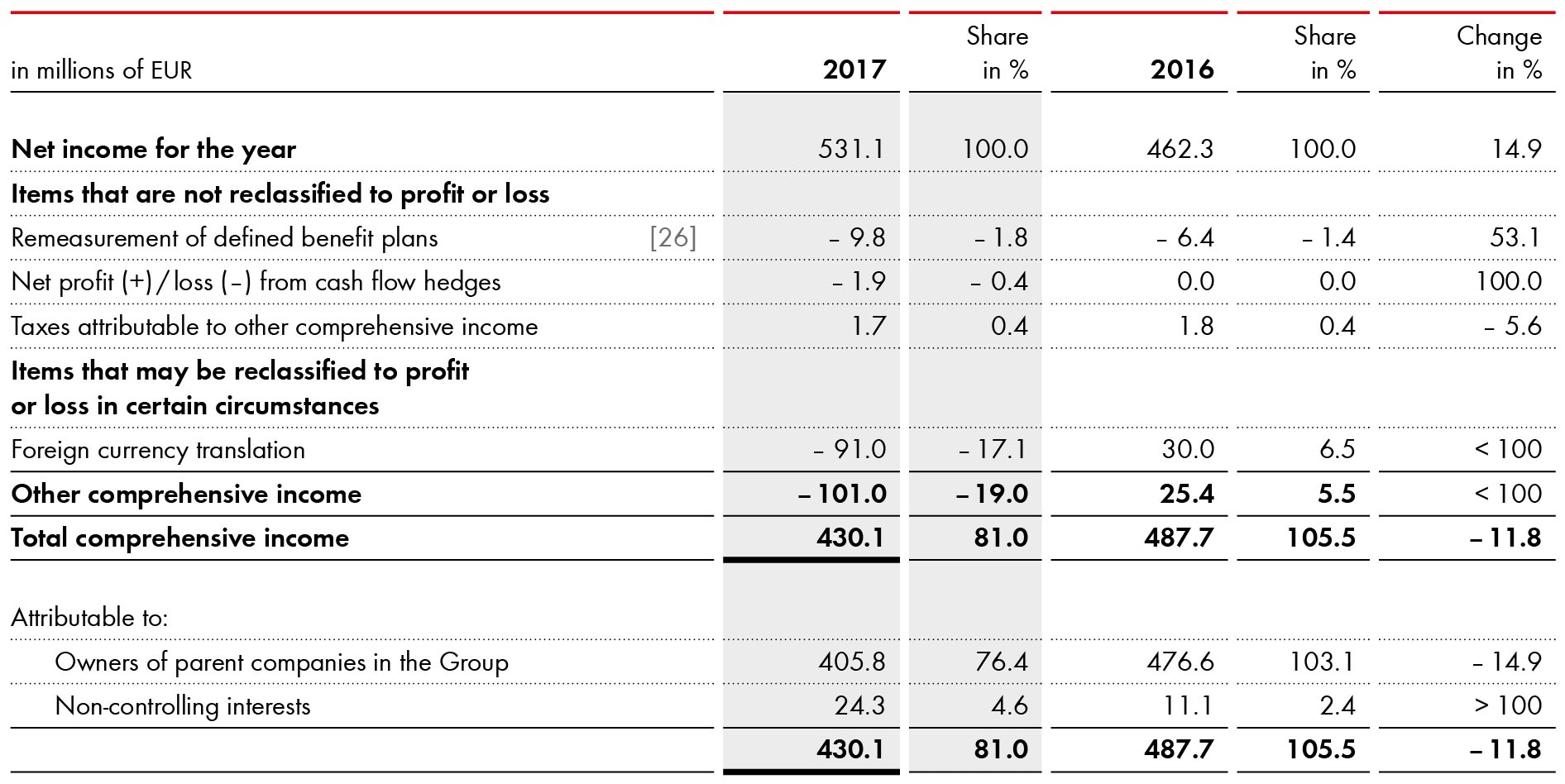

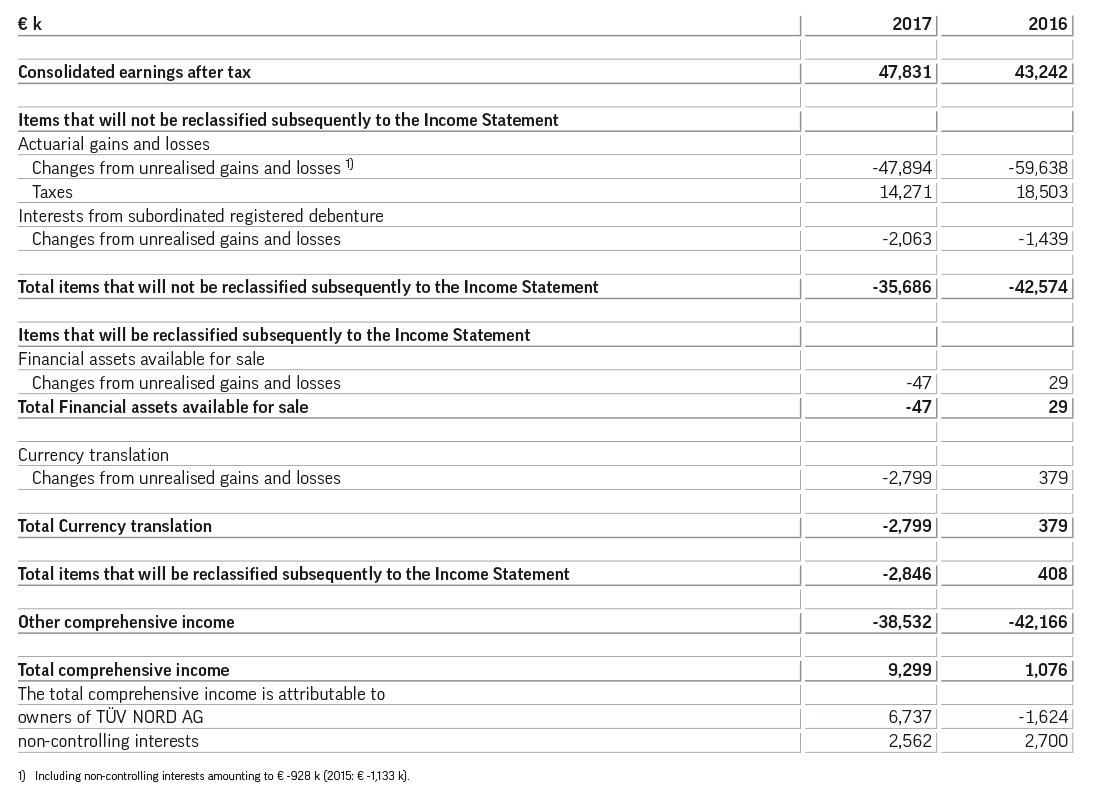

Consolidated Statement Of Comprehensive

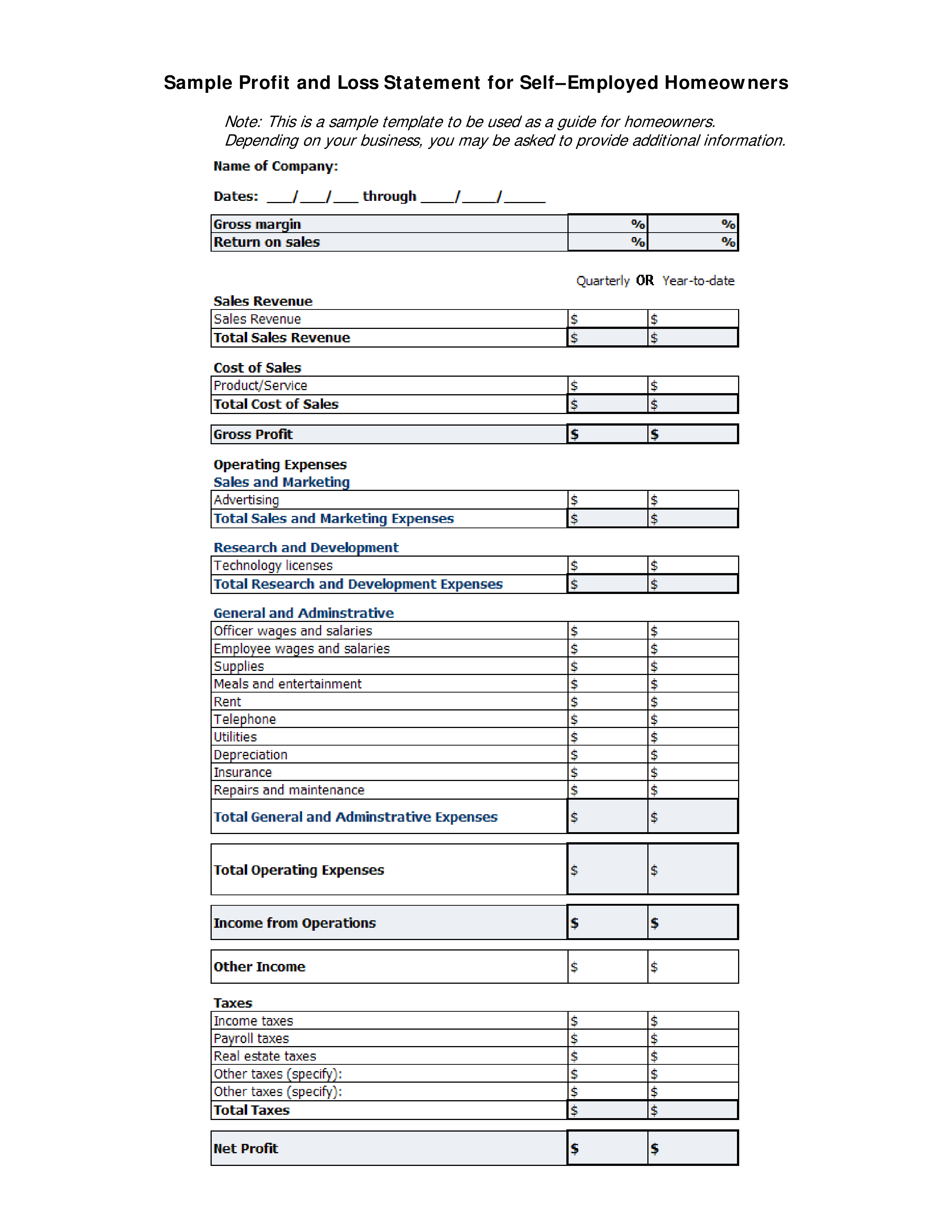

Printable Profit And Loss Statement Form Templates At

Fac1502su1format Of Statement Profit Or Loss And Other

Statement Of Comprehensive

3.4 Statement Of And Comprehensive Intermediate

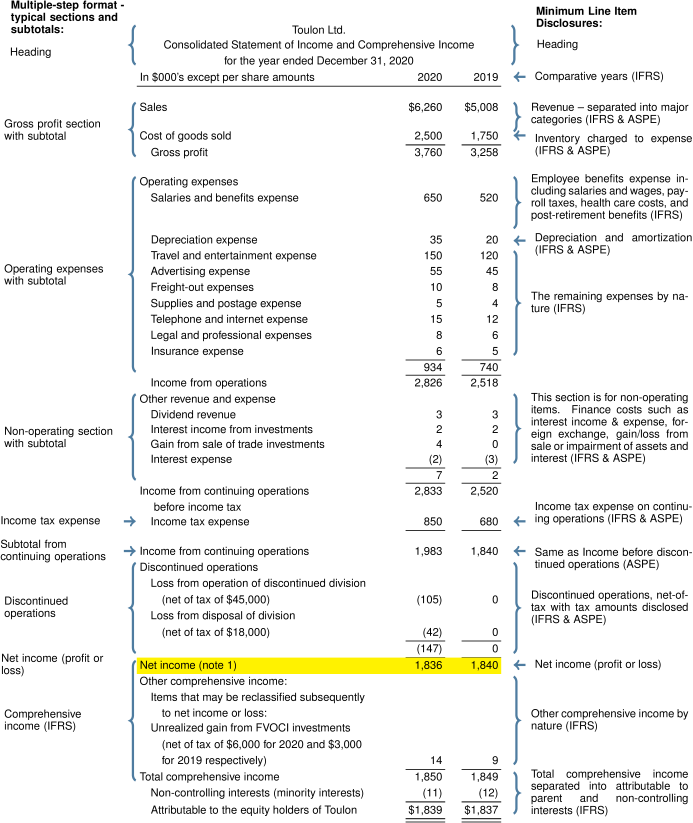

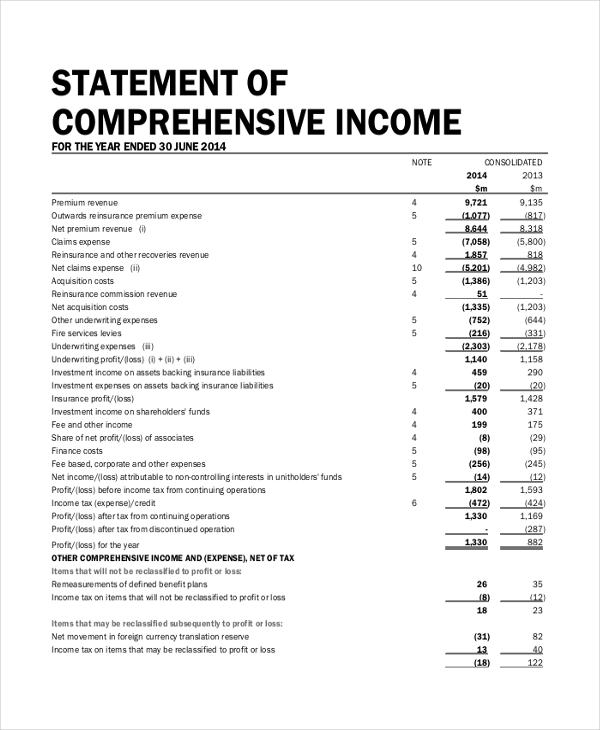

The statement of profit or loss and other comprehensive income presents all components of profit or loss and other comprehensive income in a single statement, with net income being an intermediate caption.

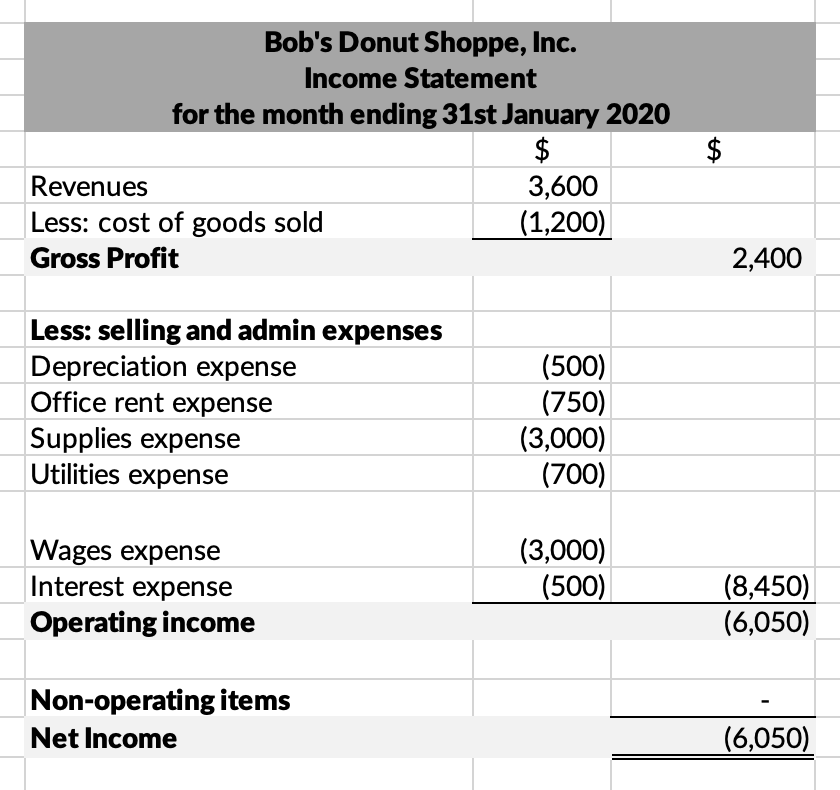

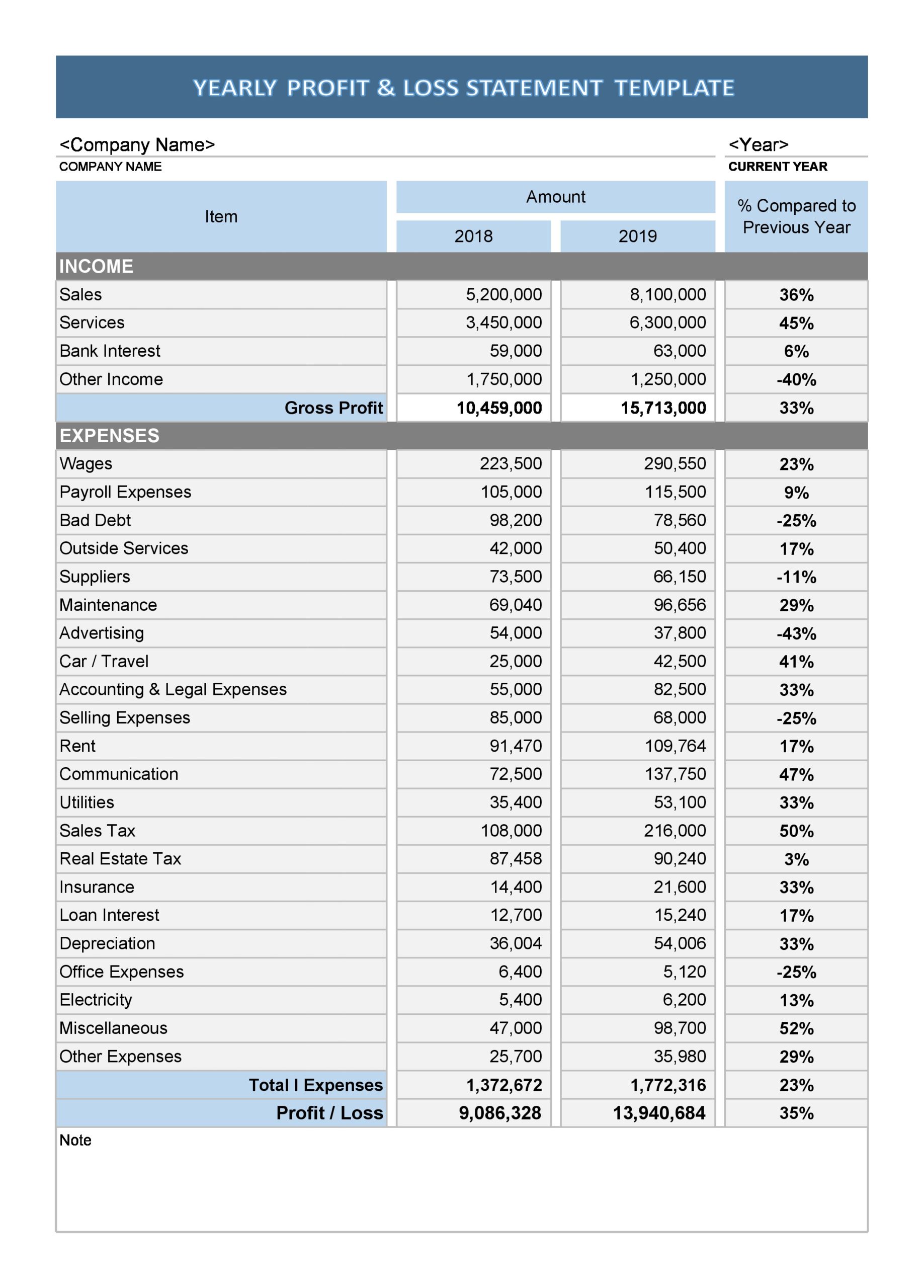

Statement of profit and loss and other comprehensive income format. Statement of changes in equity. The net income is the result obtained by preparing an income statement. Its bottom line is net income.

Other comprehensive income includes income and expenses not recognised in profit or loss such as revaluation surpluses. Other comprehensive income is those items of income and expense that are not recognised in profit or loss in accordance with ifrs standards. An entity can choose to present a single statement of profit or loss and oci or may present a statement of profit or loss and a statement of oci separately.

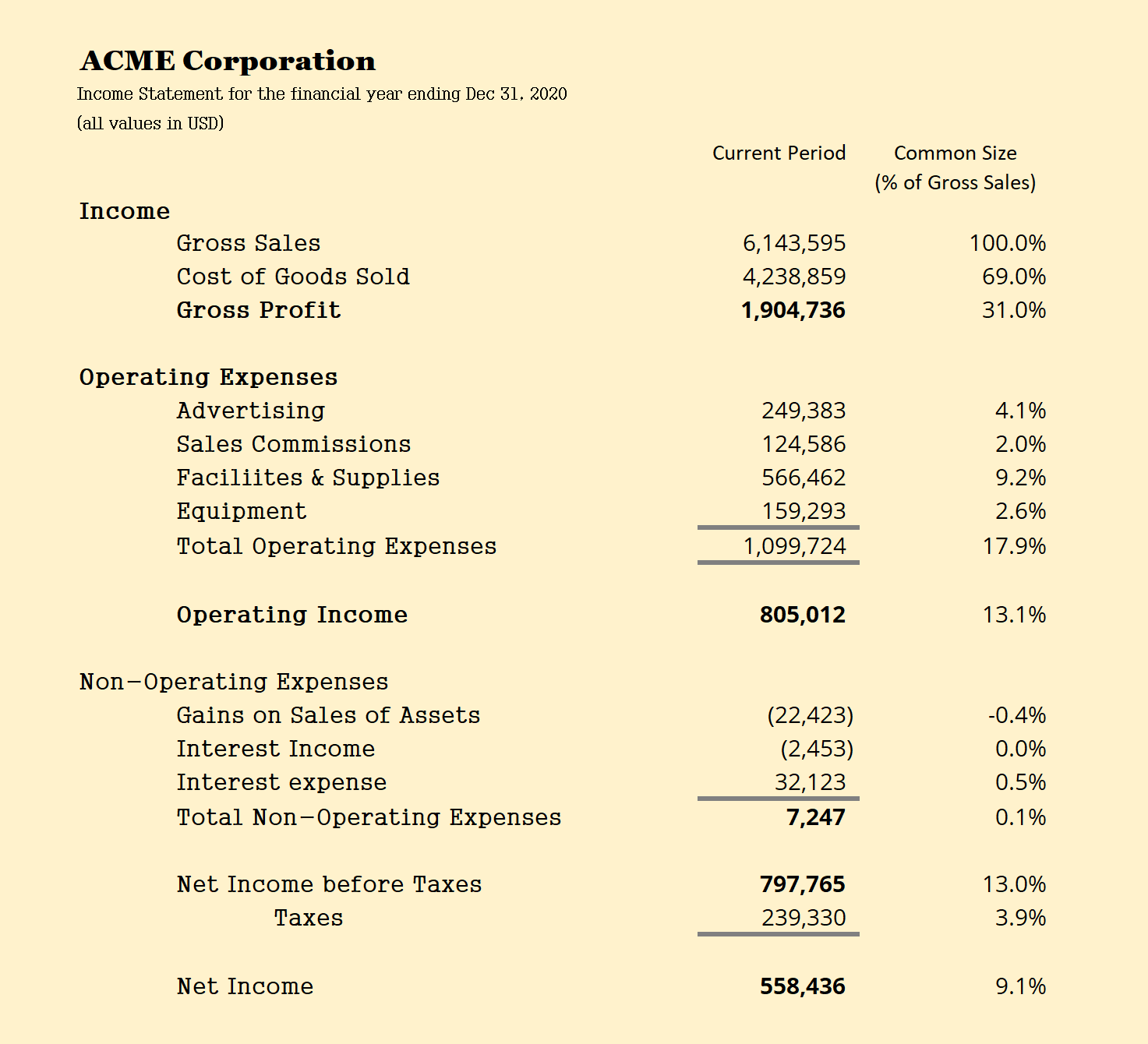

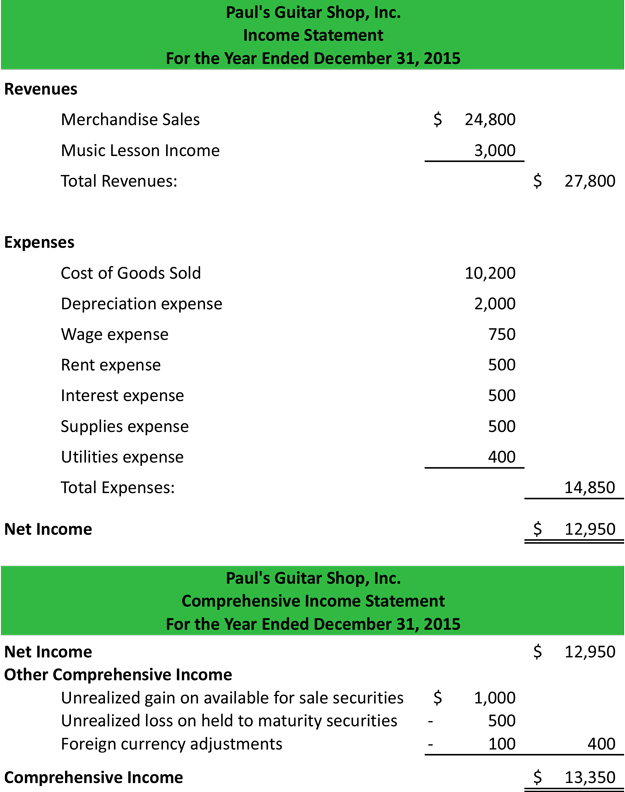

Statement of comprehensive income refers to the statement which contains the details of the revenue, income, expenses, or loss of the company that is not realized when a company prepares the financial statements of the accounting period, and the same is presented after net income on the company’s income statement. Items that will not be reclassified to profit or loss: Gross profit represents the income or profit remaining after production costs have been subtracted from revenue.

In march 2014, the staff presented to the iasb a summary of the feedback received on section 8 of the iasb discussion paper a review of the conceptual framework for financial reporting (the discussion paper)—presentation in profit or loss (p&l) and other comprehensive income (oci). The statement should be classified and aggregated in a manner that makes it understandable and comparable. A statement displaying components of profit or loss (an income statement), and a second statement beginning with profit or loss and displaying the components of oci (a statement of other comprehensive income).

What is other comprehensive income? Statement of profit or loss and other comprehensive income.

Furthermore, it allows for an indication of important trends. A statement of profit and loss and other comprehensive income for the period. The statement of comprehensive income, commonly known as the profit and loss statement, tells us whether an organization generates a profit or a loss for a period of time.

The purpose of the statement of profit or loss and other comprehensive income (oci) is to show an entity’s financial performance in a way that is useful to a wide range of users so that they may attempt to assess the future net cash inflows of an entity. Entities can either present a single statement profit or loss and other comprehensive income, or present two separate statements.

Whichever approach is adopted, both methods should arrive at total comprehensive income being the total of all component parts within the profit or loss and other comprehensive income. 5 statements of profit or loss and other comprehensive income, and changes in equity. Statement of profit or loss and other comprehensive income.

The purpose of the statement of profit or loss and other comprehensive income (ploci) is to show an entity’s financial performance in a way that is useful to a wide range of users. Ias 1 allows an entity to present a single combined statement of profit and loss and other comprehensive income or two. The statement of comprehensive income is a financial statement that summarizes both standard net income and other comprehensive income (oci).

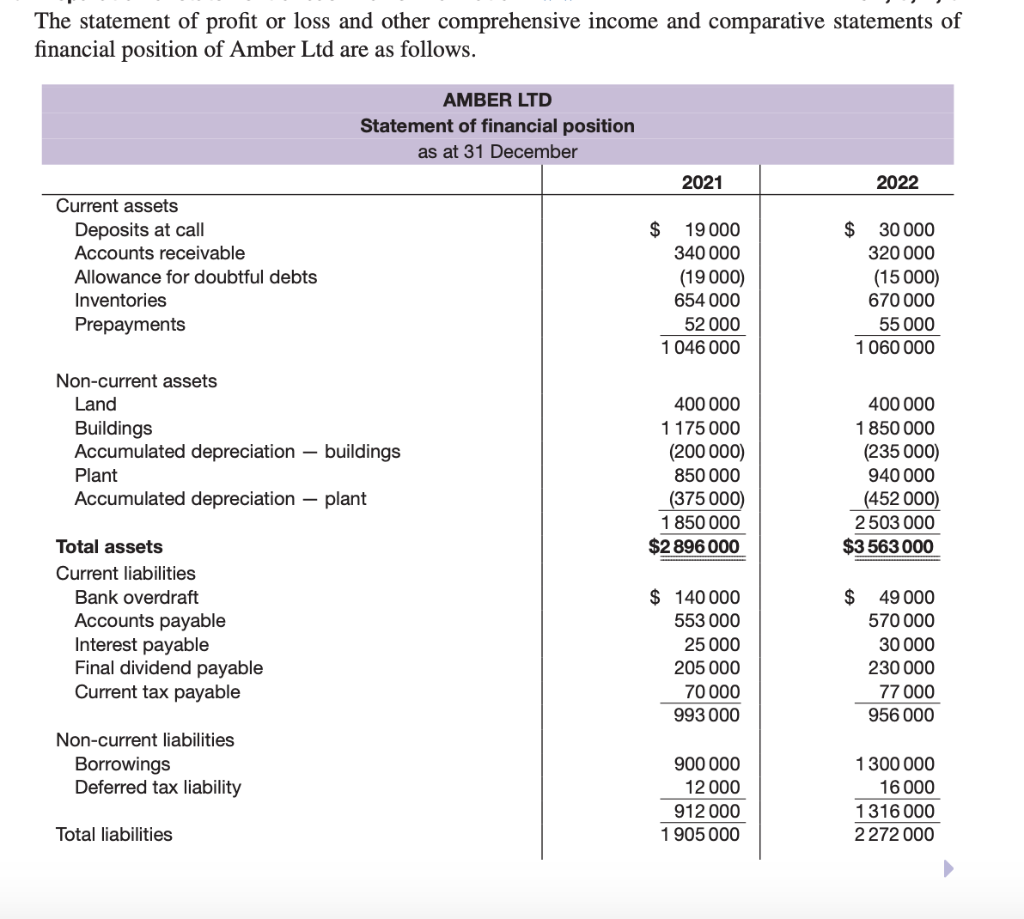

In other words, it adds additional detail to the balance sheet’s equity section to show what events changed the. Net income is the profit that remains after all expenses and costs, such as taxes.

Supreme Prepare Comparative Statement Of Profit And Loss Nike Cash Flow

How Dos A Business Use Profit And Loss Statement? Online Accounting

Comprehensive

8 Types Of P&l (profit & Loss) / Statements

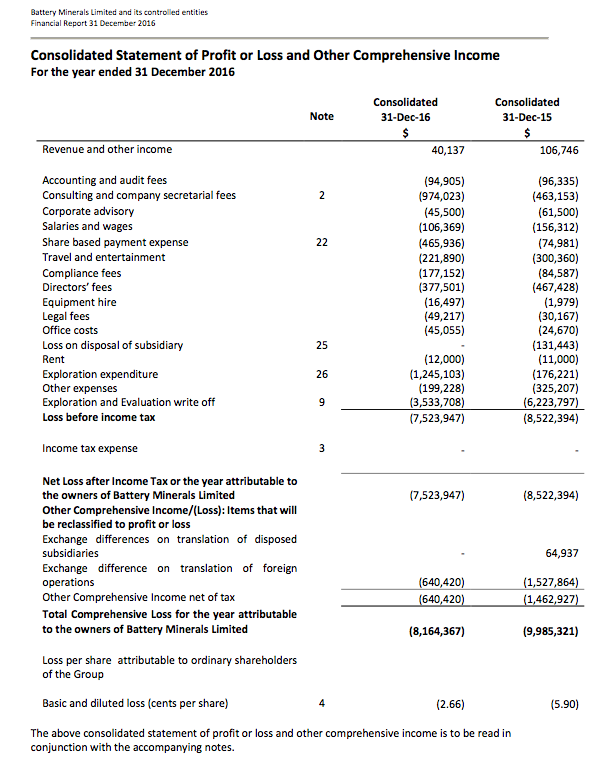

Solved Battery Minerals Limited And Its Control Led Entities

Profit, Loss And Other Comprehensive Acca Global

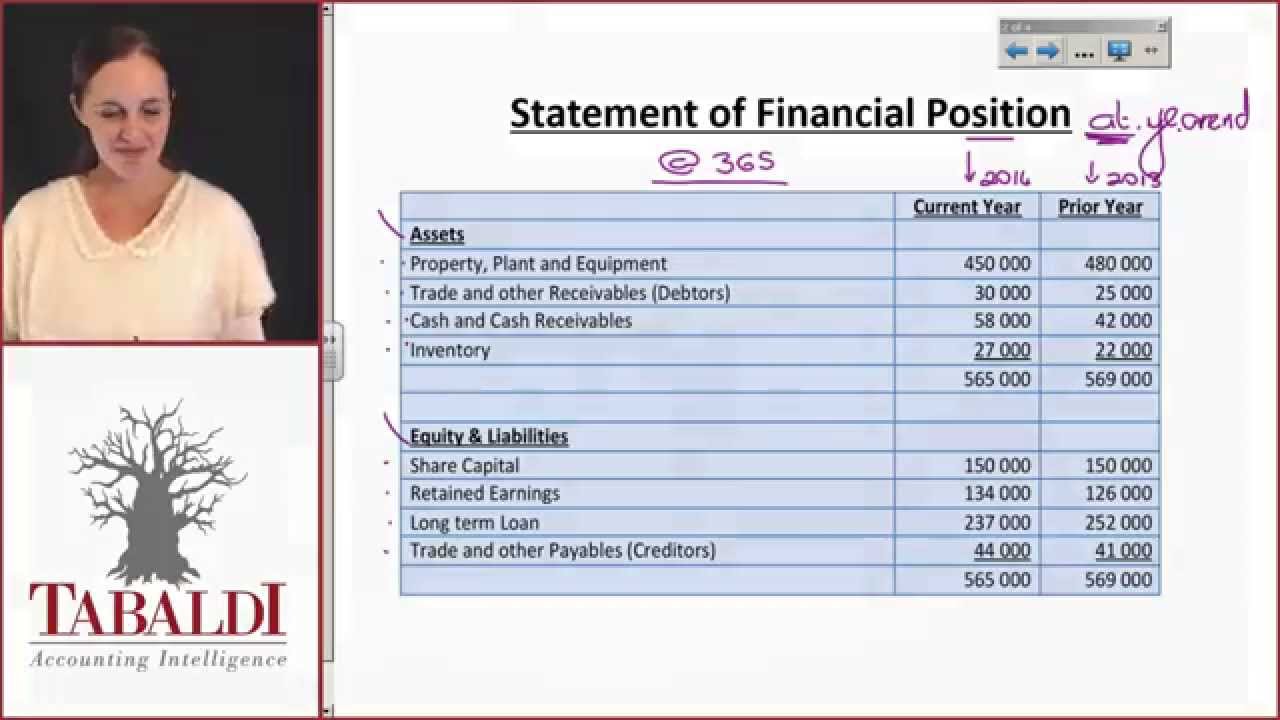

The Balance Sheet Equation Can Be Represented By All Of Following

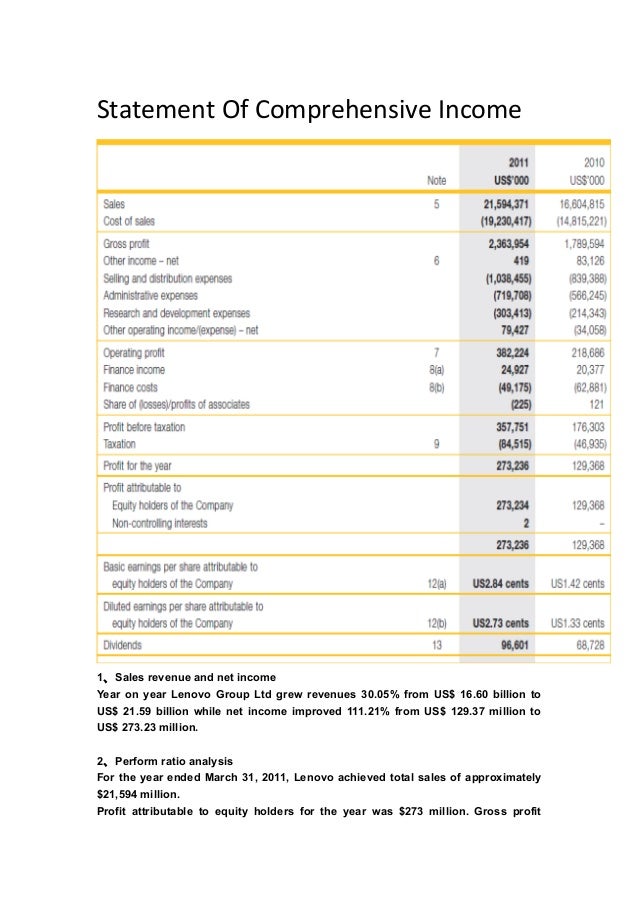

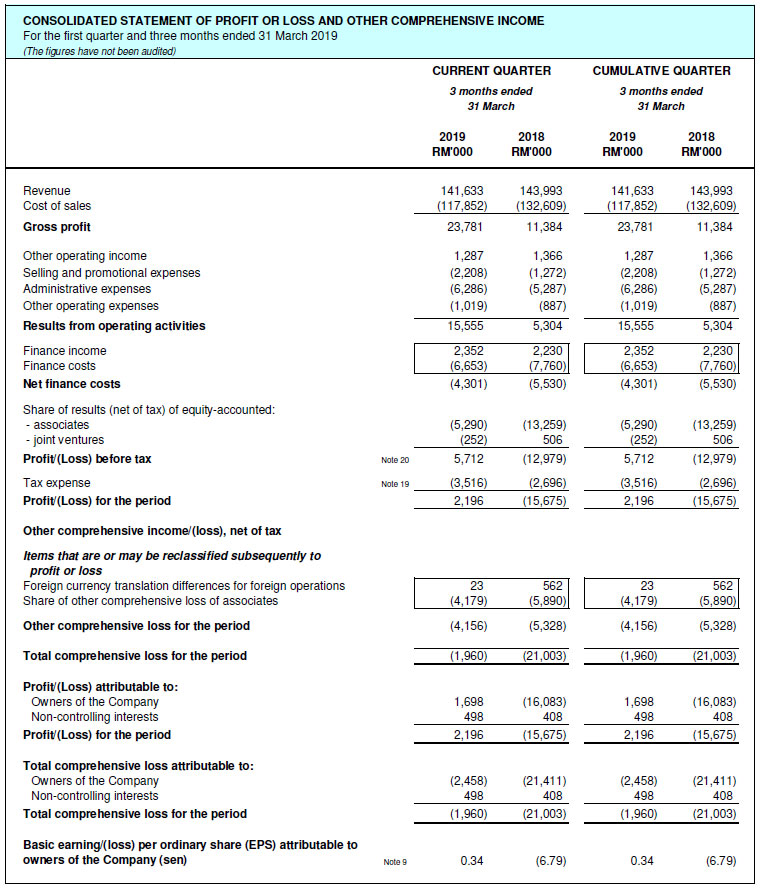

Investor Relations Financials

Fac1601su 5(ii)statement Of Profit Or Loss And Other Comprehensive

Nonprofit Profit And Loss Statement Financial Alayneabrahams

Free 10+ Sample Statement Forms In Pdf Ms Excel Word

Church Profit And Loss Statement Template

Exemplary Another Word For Net In Accounting Till Balance Sheet