Looking Good Tips About Consolidated Cash Flow Statement Eliminations

Consolidated Cash Flow Statement Of A Firm For Fy20 In One Page

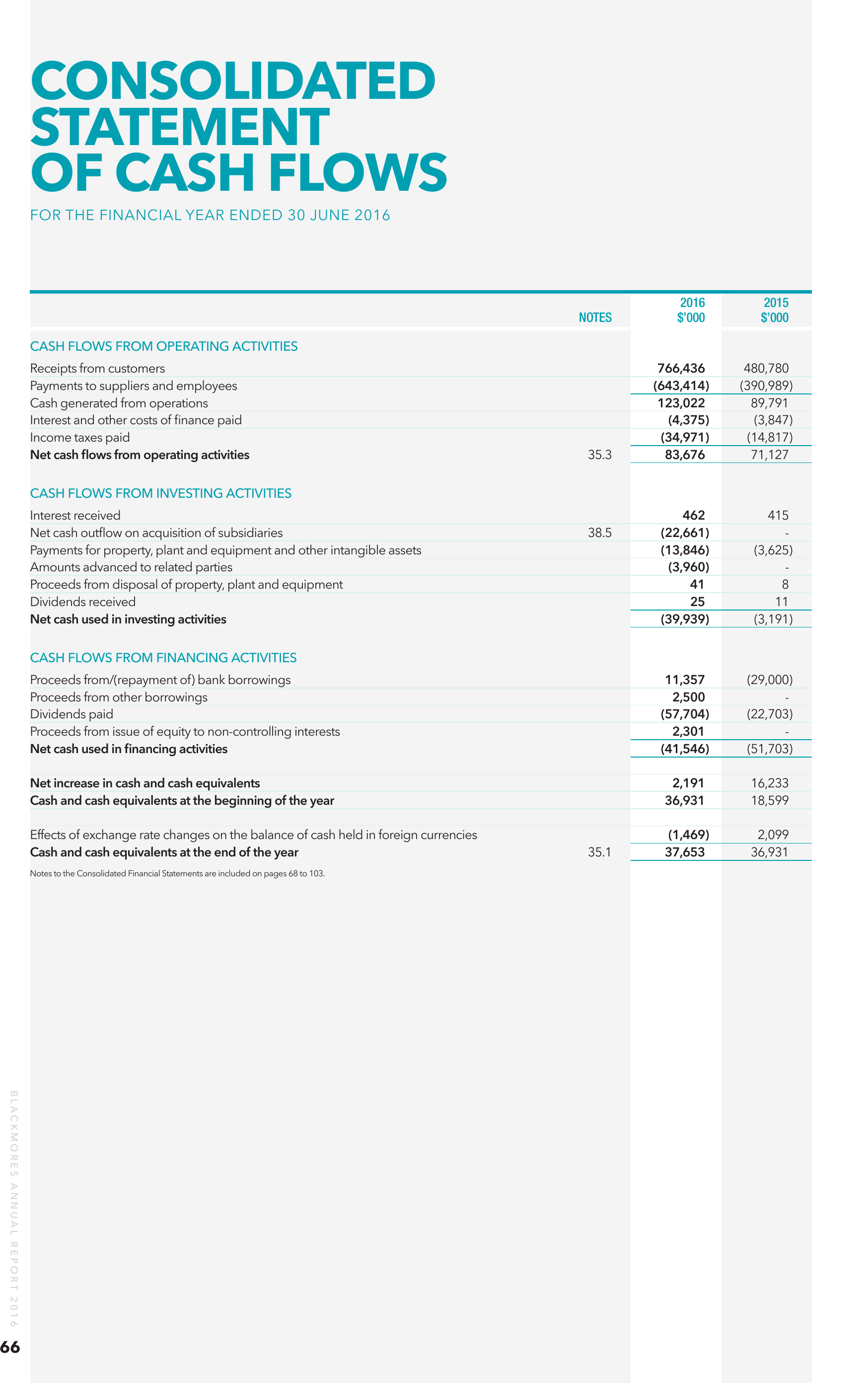

Consolidated Statement Of Cash Flows Annual Report 2016

Consolidated Statement Of Cash Flows With Foreign Currencies

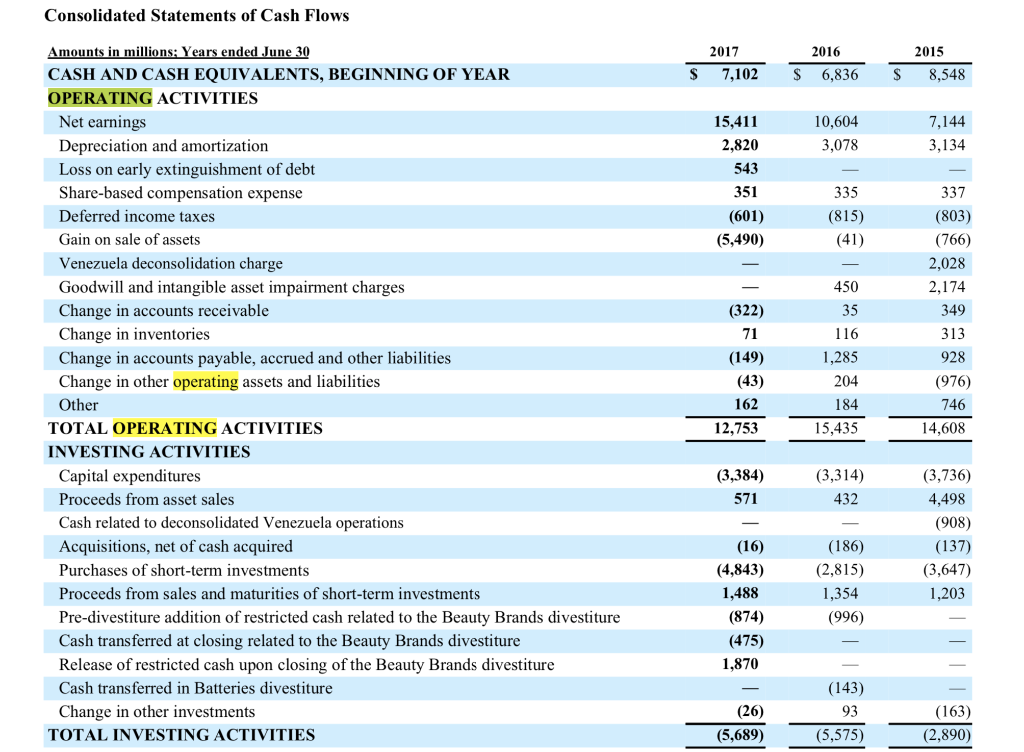

Consolidated Statements Of Cash Flows 2017 7,102 2016

One Page Consolidated Cash Flow Statement Template 162 Presentation

The consolidated statement of cash flows is not prepared from the individual cash flow statements of the separate.

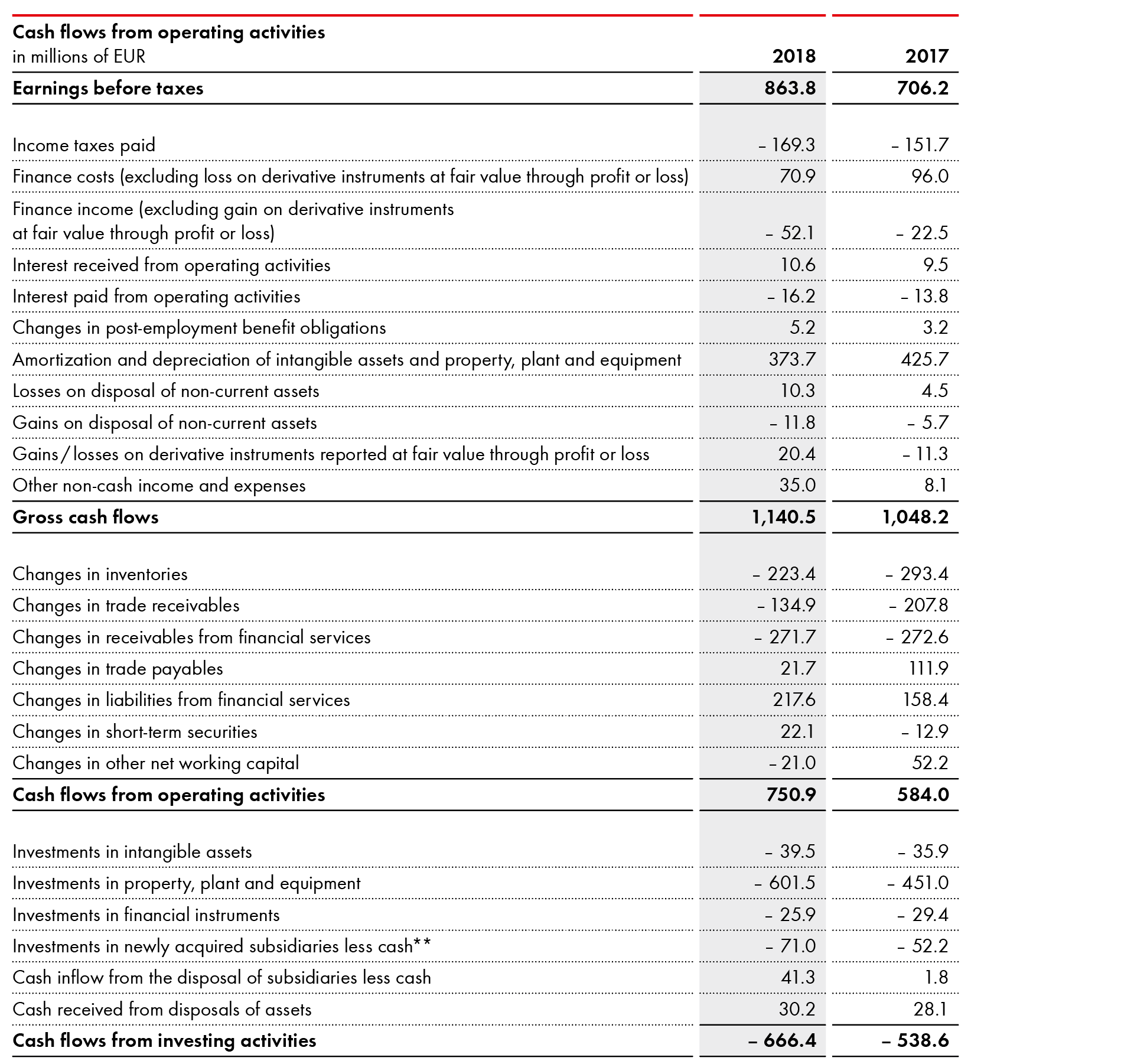

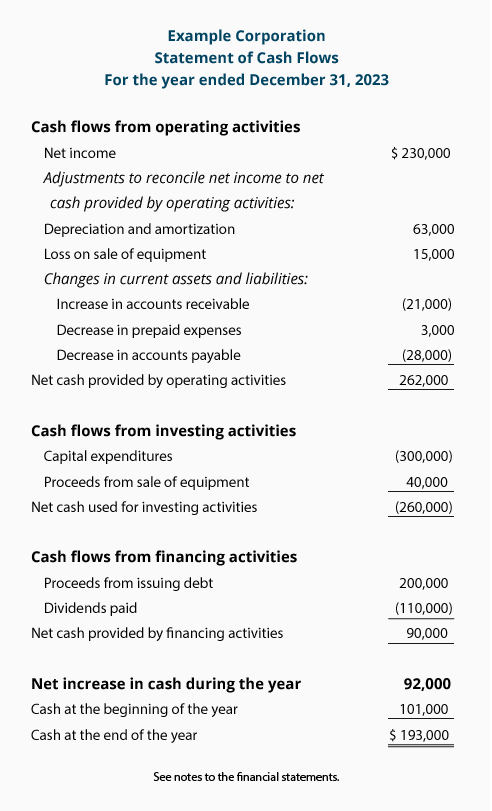

Consolidated cash flow statement eliminations. Consolidated statement of cash flows direct method 1. The above consolidated statements of cash flows should be read in conjunction with the accompanying notes. Uses and limitations of consolidated statements.

Consolidated free cash flow of € 3,885 million (2022: 95, “statement of cash flows,” mandates that companies include a statement of cash flows among their financial statements. Consolidated financial statements consist of the income statement, balance sheet and cash flow statements of a parent company and the subsidiaries.

Understand the purpose and scope. Although a business is the majority owner from pair press additional companies, a consolidated cash course statement delivers financial get in one statement. Leave the complex calculations to the software, eliminate manual tasks, and.

Before embarking on the consolidation process, it is crucial to grasp the purpose and scope of consolidated. In the consolidated financial statement, the parent and subsidiaries are treated as one entity, so all transactions between parrent and subsidiary will be. An entity can present its statement of cash flows using the direct or indirect method;

Ias 27 was reissued in january 2008 and applies to annual periods beginning on or after 1 july 2009, and is superseded by ias 27 'separate financial statements' and ifrs 10. And sub co.’s financials 100% as long as parent co. Consolidated financial statements are of primary importance to stockholders, managers, and directors of the parent company.

The latter is illustrated in. Using p&l consolidation reports with breakdown by company to streamline the monthly reporting process using p&l summary reports with monthly. Key steps in the consolidation process identify subsidiaries and prepare financial statements begin by identifying the subsidiaries that need to be consolidated.

Ias 27 defines consolidated financial statements as ‘the financial statements of a group in which the assets, liabilities, equity, income, expenses and cash flows of the parent. On the cash flow statement, you still combine parent co. Introduction this factsheet provides an overview and refresher, including practical examples and legislative references when consolidations are undertaken under frs.

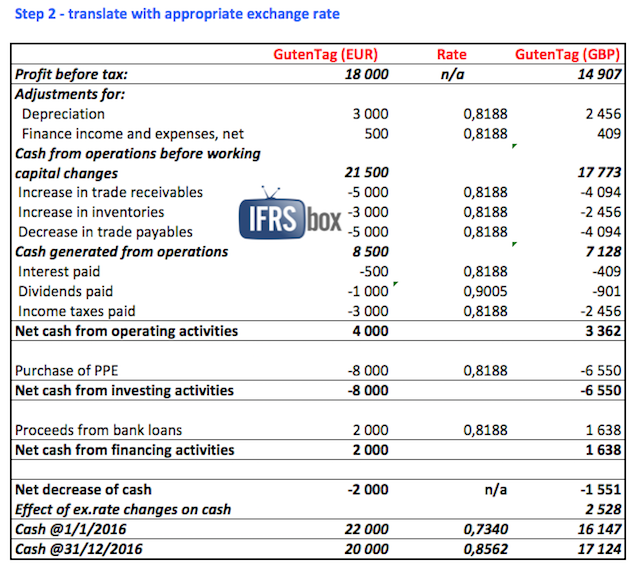

Consolidated economic statements show aggregated financial results for multiple entities or subsidiaries associated with a single sire company. The difference of €10 is a currency exchange difference which has to be adjusted in the consolidation via the following entry: The consolidation of financial statements integrates and combines all of a company's financial accounting functions to create statements that show results in.

Ifrs 10 outlines the requirements for the preparation and presentation of consolidated financial statements, requiring entities to consolidate entities it controls. Ic charge 10 => cash movement.

Consolidating Cash Flow Statement Example, Uses

One Page Consolidated Cash Flow Statement For Fy2020 Report Infographic

Cash Flow Statement Explanation And Examples Accountingcoach

Analyze Your Company’s Investing And Financing Activities For The Most

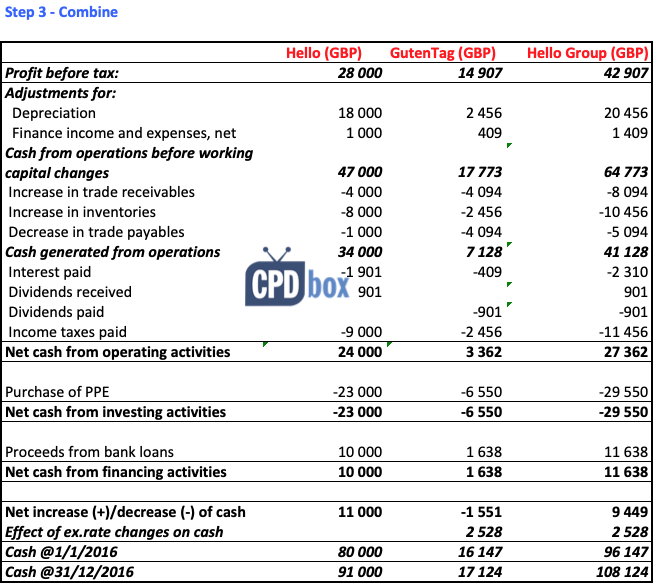

How To Make Consolidated Statement Of Cash Flows With Foreign

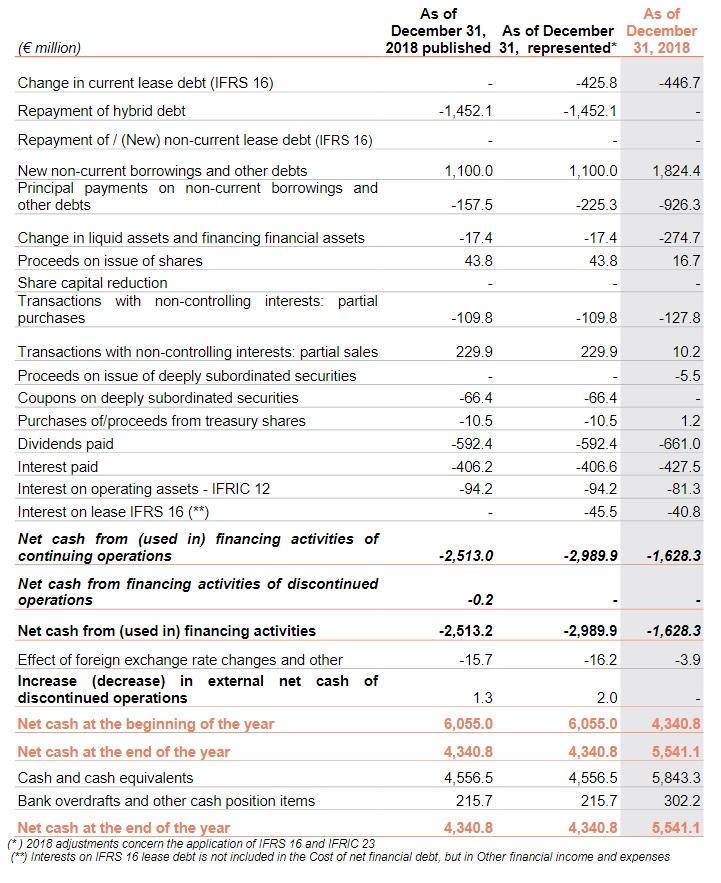

Consolidated Statement Of Cash Flows Veolia

Consolidated Financial Statements How To Better Analyse A Company

Consolidated Statement Of Cash Flows

Free 9+ Cash Flow Statement Samples In Ms Word Pdf Excel

One Page Consolidated Cash Flow Statement Of A Firm For Fy20 Template

Amazing Consolidated Cash Flow Statement Disposal Of Subsidiary Example

Consolidated Cash Flow Statement For Fy 2020 Template 61 Report